Why insurance looms so large in the climate transformation

Insurance matters because pricing risk makes an invisible reality visible

This short piece is a reflection on the role of insurance in the climate change era – in particular, insurance that accurately reflects the underlying risk.

The idea of insurance is old, going back as far as ancient Babylonia. Its more modern forms made possible early trade and other ocean expeditions. Modern property insurance first emerged in the wake of the Great Fire of London in 1666, which incinerated 13,000 homes. Following the disaster, the first fire insurance company was established.

In the wake of this first successful venture, many similar companies were founded in the following decades. Initially, each company employed its own fire department to prevent and minimize the damage from conflagrations on properties insured by them. They also began to issue 'Fire insurance marks' to their customers. These would be displayed prominently above the main door of the property and allowed the insurance company to positively identify properties that had taken out insurance with them.

…This system was soon exposed as terribly flawed, as rival brigades often ignored burning buildings once they discovered that it had no insurance policy with their company. Eventually, a solution was agreed upon in which all the insurance companies would supply money and equipment to a municipal authority charged with stationing fire prevention assets and firefighters equally around the city to respond to all fires.

Insurance transforms risk from an invisible, amorphous notion into a very real, recurring monthly expense. Once that private expense exists, minds focus and perspectives shift. In London in the late 17th century, that led to the emergence of municipal fire departments.

What might happen if everyone had to shoulder the full cost of the risks that climate-fueled weather events pose to their homes? What if it included flood risk, which has long been subsidized by FEMA’s National Flood Insurance Program (NFIP)?1

Climate adaptation efforts and, eventually, climate mitigation steps, are easy for some to reject when they’re proposed in stale political contexts, but they might land differently if people are paying high home insurance bills month after month.

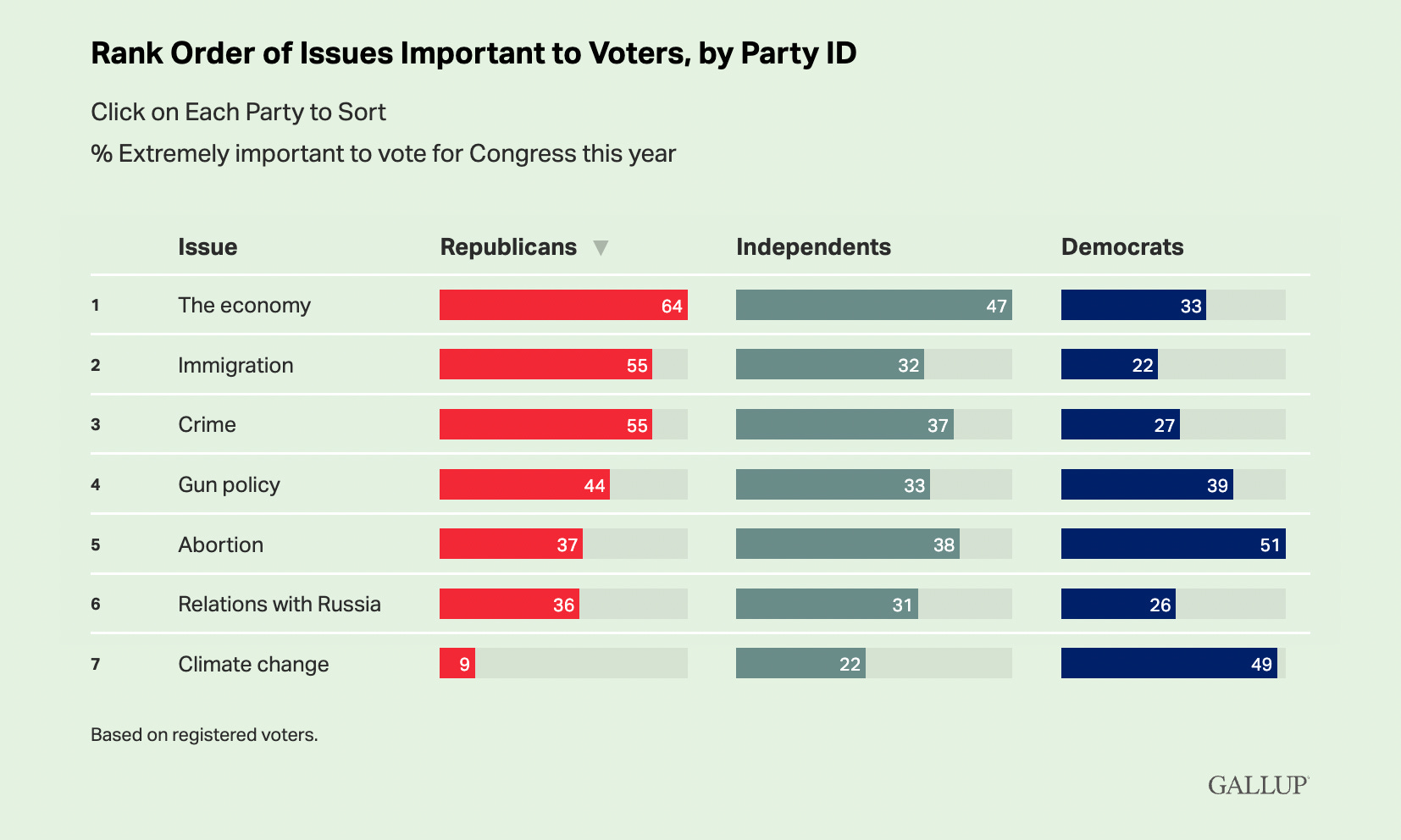

In a recent Gallup poll, just 9 percent of Republicans say climate change is “extremely important” to their congressional vote this year. That’s not from a Democratic attack ad, it’s Republican voters self-reporting!

We won’t be able to respond adequately to the climate crisis until we collectively see the problem clearly, and Republicans, as of October 2022, still don’t. That’s not a partisan statement, just a description of reality.

Their lack of concern is possible in part because climate risk can be ignored a lot of the time. Even the tens of thousands of homes on the Florida Gulf coast had been able to ignore climate change for decades. The risk of a hurricane like Ian has long been present, but for years Floridians’ luck held. Private insurance was probably underpriced, and flood insurance was (and still is) subsidized by the federal government. Because they weren’t asked to bear the cost of the risks they were taking, it was easy for people to pretend climate change was over-hyped or worse.

For a number of practical and philosophical reasons, it’s important for insurance premiums to accurately reflect the increased underlying risk from climate change:

Accurately priced insurance, by increasing the cost of ownership and thus decreasing the property value (detailed explanation here), will reduce and someday eliminate the incentives to build and re-build in climate-vulnerable locations. This practice is not only a profound waste of resources, it also results in less sophisticated consumers being financially ruined.

Rising property insurance premiums are effectively a climate impacts tax on much of the population, especially in climate vulnerable areas. This serves two functions: 1) it’s a widespread financial incentive, however modest in size, to address the root causes of climate change; and 2) it creates concrete social evidence that climate change is real, which tends to correct misperceptions and loosen the political stalemate to enable more aggressive decarbonization and other mitigation efforts.

The biggest reason human society has failed to respond adequately to the climate crisis is a failure to accurately perceive reality (see Gallup survey). Climate deniers, climate graveyard-whistlers, and doomers have been getting it wrong for at least two generations. The more misperception in the air, the further we are from ending climate change. And if insurance companies, whose job it is to understand risk, can’t see things clearly, it’s more likely average people won’t, either.

We should acknowledge it’s not easy for insurance companies to charge customers premiums that accurately reflect the true risk because the risk is a function of a rapidly-changing, highly complex climactic system. In addition to the system itself being complex, the interaction between more extreme weather and damage to manmade systems increases nonlinearly. As I noted in Insurance companies are climate change truth-tellers, Texas A&M Atmospheric Sciences professor Andrew Dessler recently described why climate impacts have spiked in recent years:

[I]f you're wondering why climate impacts seem to be getting much worse suddenly, let me introduce you to the concept of non-linearity. In a linear system, things change in straight line. If climate impacts are linear, then every 0.1°C of warming would give you the same amount of damage. In a non-linear world, on the other hand, every 0.1°C of warming produces larger damage than the previous 0.1°C. The reason for the non-linearity of climate impacts is that individuals and communities are impacted by climate when it passes thresholds. With 1.1°C of global-average warming, we are departing the climatic conditions that much of the infrastructure designed in the 20th century was designed for. Every 0.1°C of warming is going to push us past an exponentially increasing number of thresholds in the climate system.

So pricing this growing, shifting risk isn’t easy. But people bearing the full costs of their choices in the context of increasing climate risks is essential in order to make progress in the future. Insurance companies also have a clear financial incentive to get it right, and hopefully they will.

FEMA is starting to let prices increase so they come closer to reflecting actual risk, but it’s a gradual shift and one that a political revolt could still reverse at some point.